Let me start by saying: I am not a financial advisor.

But I do understand the importance of credit cards, debt management, and on-time payments when it comes to your FICO credit score.

If you’re using credit cards (and most of us are), you need to understand how they actually work—not just swipe and hope for the best.

First Things First: Budgeting Still Matters

Before we even talk about statements and APR, we have to talk about budgeting.

You must track where your money goes. Check out my previous post on Why Budgeting Matters.

It doesn’t have to be fancy. It just has to work. I personally use a spreadsheet that I constantly revise as our needs change. I’ll share it in a future post.

How I Use Credit Cards (And Why)

Full transparency:

We use credit cards for almost every purchase. I rarely use debit or ACH.

I also keep all of our cards locked and only unlock them when needed.

Yes, it’s annoying.

Yes, it’s intentional.

For example:

- Gas station sodas and energy drinks are $3+ each.

- If I stopped daily, that’s nearly $100 a month.

- Unlocking and relocking the card makes impulse spending inconvenient.

Instead, I bring my own drinks—or I wait.

Small habits matter.

Do You Actually Read Your Credit Card Statement?

You may be tracking your spending in your budget… but do you know how to read your statement?

Let’s break down what actually matters.

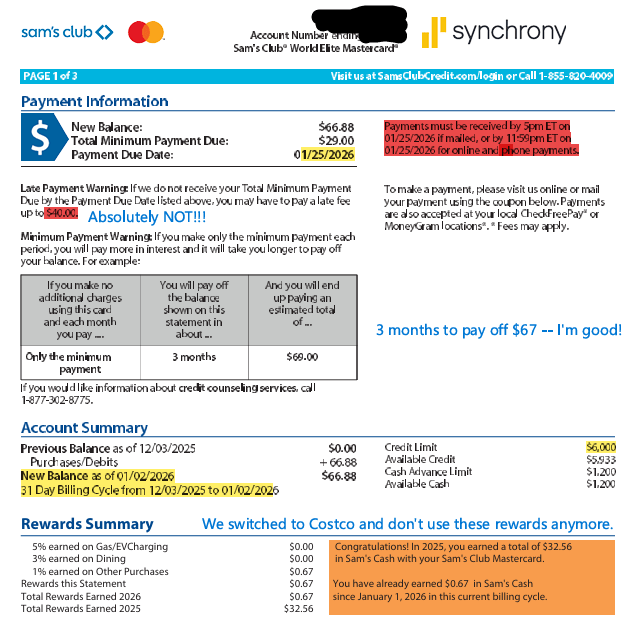

1. The Due Date (Non-Negotiable)

Example: Due Date – 1/25/2026

If you’re not tracking due dates, start immediately.

A $40 late fee is literally free money to the bank. We can’t afford that.

If you pay by mail (I pay online), the payment must be received by 5 PM on the due date. That means mailing it 10–12 business days early unless you’re paying for expedited shipping.

Also worth noting: In December 2025, USPS updated language around postmarking. Don’t assume “postmarked by” always protects you. Read the fine print on postmarking myths and facts.

2. Minimum Payment vs. Statement Balance

If your balance is $67, you probably aren’t stretching that over 3 months. But if your balance is $6,700? Different story.

Always understand:

- Minimum payment keeps you current.

- Statement balance avoids interest.

- Full current balance avoids new interest if you carry a promo.

These are not the same thing.

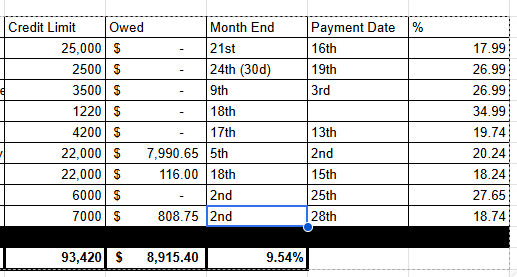

3. Know Your Billing Cycle

If you are broke, like us, this is where strategy comes in.

Your billing cycle determines your due date.

If I know a large bill is coming, I may strategically place it on a card with a later billing cycle to buy myself extra time.

For example, our car insurance was $1,117 due 2/4/2026.

If cash flow is tight, I’ll use the card whose billing cycle ends later in the month, giving me more time before payment is due.

That’s not avoiding payment—it’s managing timing. I make note of these dates on my budget. IT looks like this:

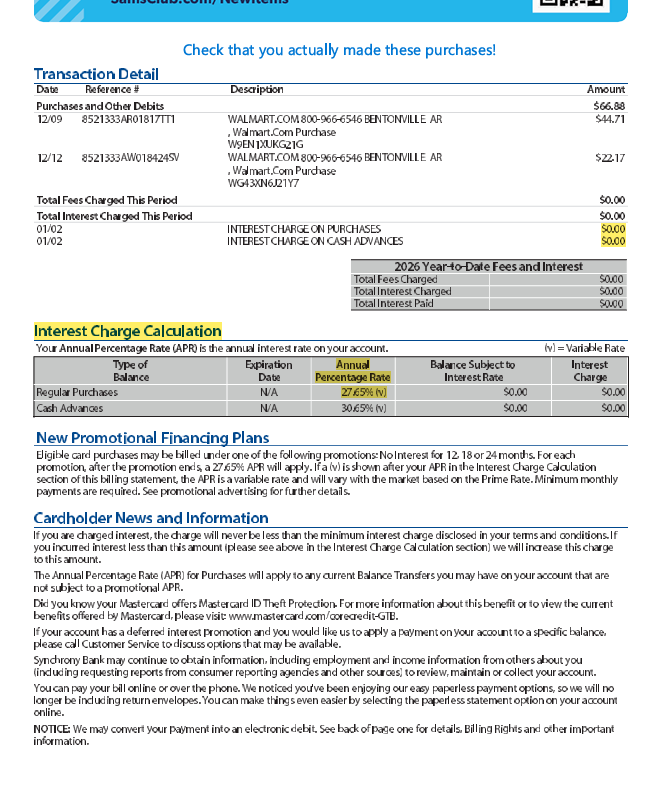

4. Review Every Charge

Every month, review your statement.

Make sure:

- You made every purchase.

- No subscriptions snuck through.

- No fraudulent charges appear.

This is one reason I prefer credit cards over debit. Fraud protection is stronger, and disputes are easier.

5. The Interest Charge Calculation Section (CRITICAL)

This section tells you:

- Your APR on purchases

- Your APR on cash advances

- How interest is calculated

- Whether you’re being charged interest this cycle

Know these numbers.

Purchase APR and cash advance APR are usually different—and cash advances are brutal. (Ask me how I know.)

If you don’t understand how interest is calculated, that’s the first thing to fix.

Why This Matters

Credit cards aren’t evil.

Misunderstanding them is expensive.

If you’re going to use credit cards:

- Track spending

- Know your due dates

- Understand billing cycles

- Read your statement

- Know your APR

- Understand payment allocation

Your money deserves your attention.

Full disclosure I wrote this originally with a very specific example in mind… and then life happened. But the core message stands:

You must understand where your money is going—especially with credit cards.

Because if you don’t understand it, the bank absolutely does.

Leave a comment